Exposing Pawram Loan App: Pawram Loan Scam Loan App

The rise of digital lending platforms has made access to personal loans easier for many, especially in a country like India, where financial inclusion is a pressing need. However, alongside legitimate platforms, there has been a surge in fraudulent loan apps that exploit vulnerable users. One such app that has recently surfaced on the Google Play Store is PawramLoan, which claims to offer “instant personal loans” without requiring income proof or a CIBIL score. While the app’s description may seem professional and compliant at first glance, several red flags suggest that PawramLoan could be a predatory scam, potentially linked to the notorious “Chinese 7-day loan apps” that have wreaked havoc in India over the past few years. In this article, we will expose the dubious practices of PawramLoan, analyze its claims, and highlight the risks associated with using such apps.

What is PawramLoan?

According to its Play Store description, PawramLoan markets itself as a “fast, transparent, and digital lending platform for India.” It claims to be developed by PAWRAM TRADING PRIVATE LIMITED, a technology and service platform provider, while loans are supposedly disbursed by their registered NBFC partner, Udvai Traders Private Limited, in compliance with RBI guidelines. The app promises loans ranging from ₹2,000 to ₹100,000 with tenures of 90 to 120 days, quick approvals, and a fully digital process with no paperwork. It also mentions eligibility criteria, such as being an Indian citizen over 18 years old with a valid PAN, Aadhaar, and an active bank account.

At first glance, the description appears legitimate, with mentions of RBI compliance, transparent terms, and a structured loan calculation. However, the claim of providing loans “without income proof or CIBIL score,” as seen in the promotional image, raises serious concerns. Let’s break down why PawramLoan may not be what it seems.

Red Flags: Why PawramLoan Could Be a Scam

- Claims of Loans Without CIBIL or Income Proof

Legitimate financial institutions, including RBI-registered NBFCs, are required to perform due diligence before disbursing loans. This includes verifying the borrower’s creditworthiness through a CIBIL score or other credit evaluation mechanisms, as well as ensuring a stable source of income to assess repayment capacity. PawramLoan’s claim of offering loans without these checks is highly suspicious. Such practices are often associated with predatory loan apps that target desperate individuals, only to trap them in a cycle of debt with exorbitant interest rates and hidden fees. - Short Loan Tenure and High Fees

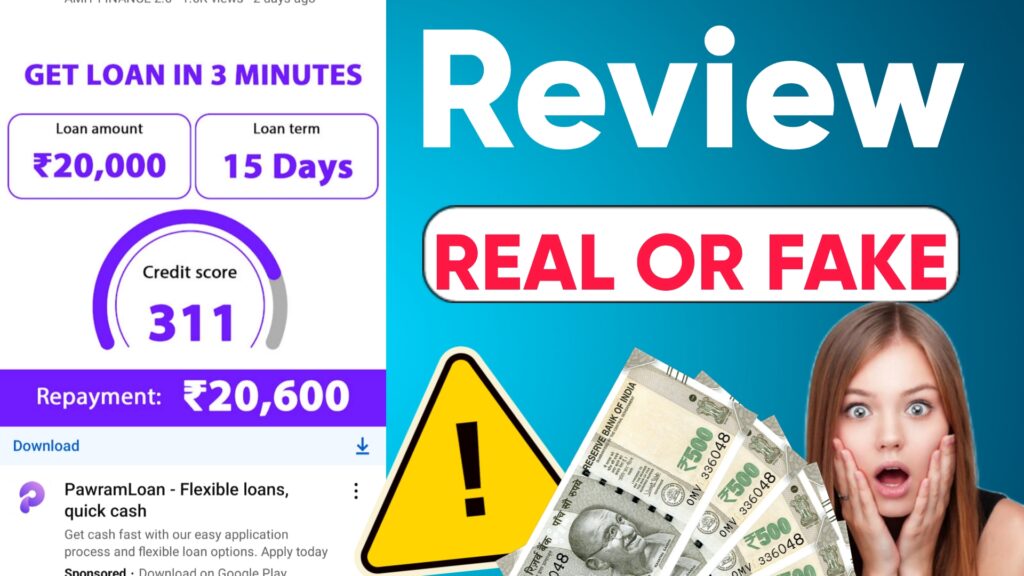

The Play Store description mentions loan tenures of 90 to 120 days, but the promotional image in the user’s screenshot shows a loan term of just 15 days for a ₹20,000 loan, with a repayment amount of ₹20,600. This indicates a daily interest rate that is extremely high for such a short period. Additionally, the app charges a processing fee (5-6%), a documentation fee (1%), a convenience fee (₹200), and GST (18% on all fees). For a ₹30,000 loan, the total deductions amount to ₹2,360, leaving the borrower with only ₹27,640 in hand while requiring a repayment of ₹33,710 in just 90 days. These high fees and short tenures are classic tactics used by Chinese 7-day loan apps to exploit borrowers. - Potential Chinese Loan App Connection

Between 2019 and 2021, India saw a wave of fraudulent loan apps linked to Chinese operators. These apps, often referred to as “7-day loan apps,” offered short-term loans with minimal documentation but charged exorbitant interest rates (sometimes as high as 1% per day). They were notorious for harassing borrowers, accessing their personal data (like contacts and photos), and using blackmail tactics to enforce repayment. While PawramLoan claims to be operated by an Indian company (PAWRAM TRADING PRIVATE LIMITED) with an NBFC partner (Udvai Traders Private Limited), the lack of transparency about its operations and the similarity of its loan terms to those of Chinese loan apps raise serious doubts about its legitimacy. - Low Credit Score in Promotional Image

The screenshot shared by the user shows a credit score of 311, which is extremely low (CIBIL scores typically range from 300 to 900, with anything below 600 considered poor). Legitimate lenders would not approve a loan for someone with such a low credit score, especially without additional documentation or collateral. This suggests that PawramLoan may be targeting financially vulnerable individuals who are unlikely to qualify for loans from regulated institutions. - Harassment Concerns

The search query in the screenshot, “pawramloan app harassment,” indicates that users may already be experiencing issues with the app. Chinese loan apps were infamous for their aggressive recovery tactics, including sending threatening messages, morphing photos of borrowers, and contacting their family and friends to shame them into repayment. If PawramLoan is engaging in similar practices, it could be a significant risk to users’ privacy and mental well-being. - Lack of Verifiable Information

While the app mentions its NBFC partner, Udvai Traders Private Limited, there is no easily accessible public information to verify the legitimacy of this entity or its RBI registration. PAWRAM TRADING PRIVATE LIMITED also lacks a well-established digital footprint, which is unusual for a company claiming to provide financial services. Legitimate lending platforms typically have a transparent online presence, including a website, customer support channels, and verifiable reviews.

The Risks of Using PawramLoan

Using an app like PawramLoan can expose users to several risks:

- Data Privacy Violations: Fraudulent loan apps often request excessive permissions, such as access to contacts, photos, and location data. This information can be misused for blackmail or sold on the dark web.

- Financial Exploitation: High interest rates and hidden fees can trap users in a debt cycle, making it impossible to repay the loan without borrowing more.

- Harassment and Mental Stress: If the app engages in aggressive recovery tactics, users may face harassment, threats, and public humiliation.

- Legal Issues: If the app is not genuinely compliant with RBI regulations, users may inadvertently get involved in illegal financial transactions.

How to Protect Yourself from Fraudulent Loan Apps

- Verify the Lender: Always check if the lender is an RBI-registered NBFC or bank. The RBI maintains a list of registered NBFCs on its website.

- Read Reviews and Research: Look for user reviews and news articles about the app. If there are reports of harassment or fraud, steer clear.

- Check Loan Terms: Be wary of apps that offer very short loan tenures, high interest rates, or claim to provide loans without any credit checks.

- Limit Permissions: Avoid granting unnecessary permissions to loan apps, such as access to your contacts or photos.

- Report Suspicious Apps: If you suspect an app is fraudulent, report it to the Google Play Store and local authorities, such as the cybercrime cell.

FAQs About PawramLoan

Q1: Is PawramLoan a legitimate loan app?

A: While PawramLoan claims to partner with an RBI-registered NBFC (Udvai Traders Private Limited), its claims of providing loans without CIBIL or income proof, along with its high fees and short loan tenures, raise serious doubts about its legitimacy. It may be linked to predatory Chinese loan apps.

Q2: What are the loan terms offered by PawramLoan?

A: According to its Play Store description, PawramLoan offers loans from ₹2,000 to ₹100,000 with tenures of 90 to 120 days. However, the promotional image shows a 15-day tenure for a ₹20,000 loan, with a repayment of ₹20,600, indicating high interest rates and fees.

Q3: Can I trust PawramLoan with my personal information?

A: Given the app’s questionable practices and potential links to Chinese loan apps, there is a high risk of data misuse. Users should avoid sharing sensitive information like PAN, Aadhaar, or bank details with this app.

Q4: What should I do if I’ve already taken a loan from PawramLoan?

A: If you’re facing harassment or suspect foul play, stop engaging with the app, report it to the authorities (such as your local cybercrime cell), and seek legal advice. Do not pay additional fees or interest without verifying the app’s legitimacy.

Q5: How can I identify a fake loan app?

A: Look for red flags like promises of loans without credit checks, high interest rates, short repayment periods, and lack of transparency about the lender’s registration. Always verify the lender’s credentials with the RBI.

Conclusion

PawramLoan may present itself as a convenient solution for quick cash, but its dubious claims, high fees, and potential links to Chinese 7-day loan apps make it a risky choice for borrowers. The app’s promise of loans without CIBIL or income proof, combined with reports of harassment (as suggested by the user’s search query), strongly indicates that it could be a scam designed to exploit vulnerable individuals. If you’re in need of a loan, opt for well-known, RBI-registered financial institutions or NBFCs with a proven track record. Stay informed, stay cautious, and protect yourself from the growing threat of fraudulent loan apps like PawramLoan.